|

|

|

The Market Monitor

|

Silicon Valley Bust

A month ago, as we looked ahead to the remainder of the first quarter and thought about the issues technology company management teams were most likely to face in the coming weeks, our conclusions were pretty standard. On the macro front, we thought inflation would continue to be the primary issue on everyone’s minds, while from a fundamental perspective we thought the cautious IT spending environment and its impact on revenue growth (due to elongated sales cycles, added levels of scrutiny on larger deals, prioritization of projects with rapid payback, etc. that we had been hearing about) would remain the primary area of concern.

|

We were as blindsided as the rest of the world by the sudden collapse of Silicon Valley Bank (SVB), an event without precedent in Silicon Valley and the second-largest bank failure in U.S. history. Suddenly, the main question on investors’ minds rapidly shifted to whether companies had deposits at the bank and what their exposures were. While the financial regulators rapidly stepped in to guarantee non FDIC-insured deposits and minimize market disruption, many believe the impact of the failure of SVB, the subsequent banking crisis which led to the failure of Signature Bank, and the contagion that resulted in the Swiss government-backed takeover of Credit Suisse by UBS, will have lasting implications. In an environment of heightened risk, banks are expected to pull back on lending, which is expected to negatively impact economic growth.

|

Perhaps surprisingly technology stocks were among the best-performing assets in the wake of a Silicon Valley-based crisis, ending the month of March 7% higher and for the first quarter up 17%. By the end of the quarter, the NASDAQ had entered a bull market for the first time in nearly three years, with the benchmark up 20% relative to its closing price on December 28th. This was powered in part by megacaps Apple, Amazon, and Microsoft, as well as a broader rebound in beaten-down high-growth tech stocks. The banking crisis turned out to have a silver lining for tech stocks as the market dialed back expectations for additional rate hikes. Tech stocks are more sensitive than average to rates as a higher share of their theoretical market value is based on earnings forecasted to materialize in the distant future. The present value of these earnings is highly sensitive to the discount rate, and it is therefore no surprise that the most speculative stocks have been hit the hardest since the current interest rate cycle began.

|

In spite of the recent rally in tech stocks, equity capital markets activity remains light and the IPO window remains effectively closed. Yet with venture capital and other private sources of market funding drying up and private owners increasingly marking down their companies to reflect public market realities, many cash-burning private technology companies face the prospect of raising new money at a steep discount to their most recent funding round. The private markets no longer represent a safe harbor as they have for the past few years, which is leading companies to focus on generating positive organic free cash flow as though their lives depended on it. For many, that may prove to be the case.

|

On the political front, the third year of the presidential cycle is unfolding in an unprecedented manner with the indictment of Donald Trump by a Manhattan grand jury. The indictment incited strong reactions on both sides of the political spectrum, and it remains unclear whether it will ultimately help or harm Trump’s 2024 Presidential bid. Regardless, we are hopeful that the presidential election cycle theory will play out, and the market will continue its upward march through year-end.

|

|

We hope you enjoy reading this month’s Monitor and pass it along to others to subscribe. Happy reading!

|

|

|

|

|

|

- See You Later, Alligator. Tampa police officers were called to a commercial part of town because of a disturbance, but it wasn’t a public brawl or anyone behaving in a disorderly manner. It was a 9-foot alligator ambling down the street. The urban gator whipped its tail several times when an officer first approached it, poking with an outstretched baton. A half dozen officers along with a crowd of spectators watched as lights from squad cars flashed on the blocked off street. To restrain the rowdy creature, three officers were needed: one went for the head with outstretched hands while two others weighed down the rest of the alligator’s body. The officer keeping the gator’s mouth shut asked his colleagues for a towel to cover its eyes and some duct tape to wrap its mouth. They also taped together the gator’s legs. “Behind his back, like you’re handcuffing him,” an officer said. Mission: Accomplished.

- Oh, Dear. A man in York County, Pennsylvania, was arrested after allegedly leading officers on two separate vehicle chases in two counties. Tony Saunders was pulled over in a BMW after officers spotted him driving with items that appeared to be from a nearby convenience store where a theft had been reported. Saunders reportedly told police he got the items at a junkyard. There was also reportedly a dog in the vehicle and a dead deer in the trunk. Saunders successfully evaded the police, although later that morning local law enforcement agencies were notified that a school bus had been stolen in Abbottstown. Police apprehended and identified the driver as Saunders, who allegedly admitted he had stolen the school bus after crashing the BMW. He also allegedly claimed he intended to use the dead deer carcass to fertilize his garden. Apparently Home Depot is running low on fertilizer!

- Musical Notes on a Scandal. A Flemish family in Belgium who shares a last name with Ludwig van Beethoven and had proudly claimed to be related, was recently devastated to learn that they had no genetic ties to him. Others were dismayed to find that a lock of hair believed to have belonged to the composer actually came from an Ashkenazi Jewish woman, while backers of theories that Beethoven had lead poisoning or was a Black man were sorely disappointed. These disappointments came about as a result of a new report based on the analysis of strands of Beethoven’s hair which also provides an explanation for his debilitating ailments and even his death, while also raising new questions about his genealogical origins and hinting at a dark family secret. As it turns out, Beethoven’s father was likely the product of an extramarital affair. With DNA, no secrets are safe!

- Monkey Business. HelloFresh, the German meal kit company, announced it would stop using coconut milk from Thailand this year, after allegations by the animal rights advocacy group PETA of the use of forced monkey labor in the coconut industry there. The decision was made in December and was made public last week. Walmart, Costco and other large American retailers have also halted sales of Chaokoh coconut milk, a Thai brand, but HelloFresh has pledged to stop using coconut milk from Thailand entirely. PETA has long claimed that monkeys in Thailand are forced to climb tall trees for hours and to pick coconuts that will be used to make products such as coconut milk, flour and oil. Looks like the game is up, and there will be no more monkeying around for HelloFresh and other conscientious retailers!

|

|

|

|

|

Image of the Month

|

|

|

|

A Brinks worker walks toward a truck after exiting Silicon Valley Bank in Santa Clara, Calif., Friday, March 10, 2023.

|

|

|

|

Image Credit: AP Photo/Jeff Chiu.

|

|

|

|

Chart Series

|

|

|

|

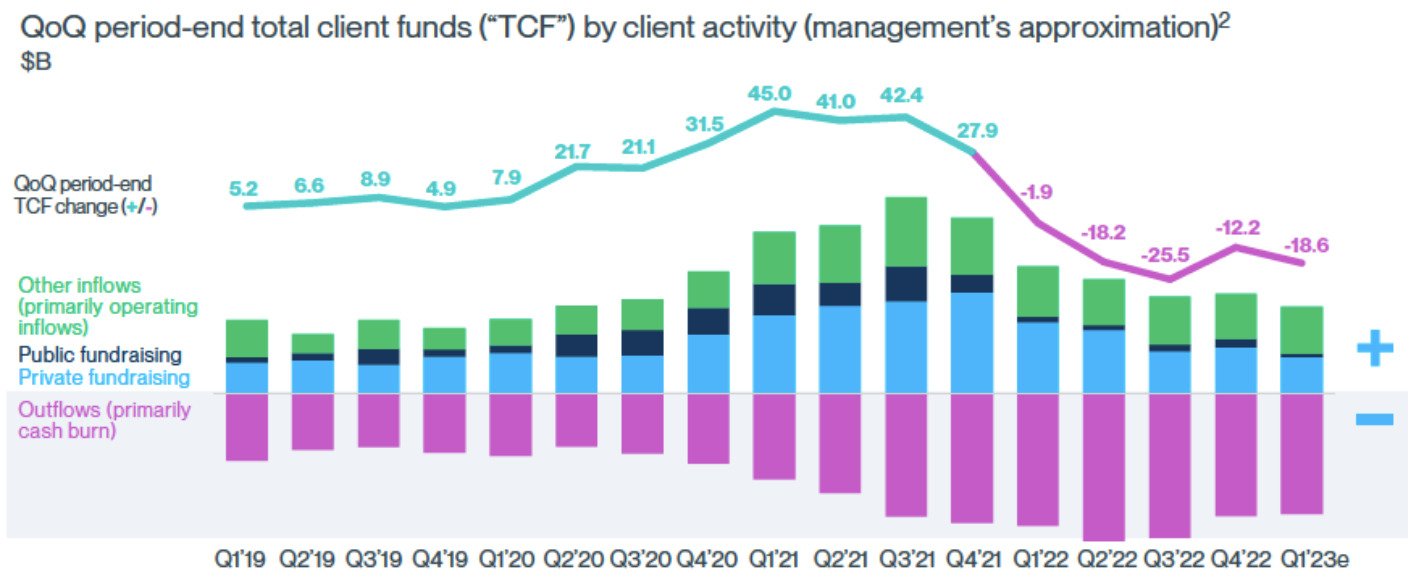

Silicon Valley Bank’s Waning Client Funds. For four consecutive quarters prior to its collapse, Silicon Valley Bank faced declining client funds balances, as new VC funding fell short of cash burn for the bank’s VC-backed technology and biotech clientele.

|

|

|

|

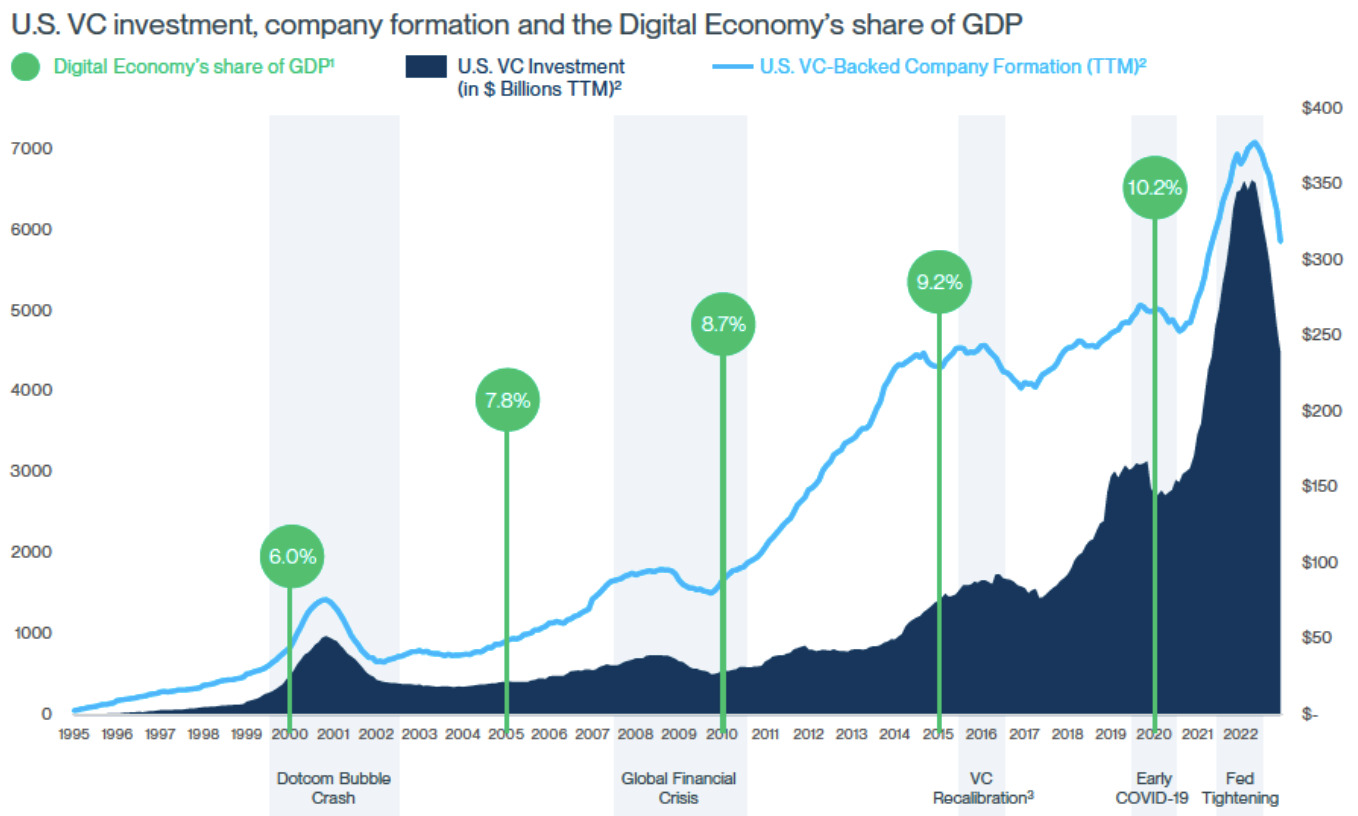

The Latest VC Bubble. After the largest run-up in venture capital funding since the Dotcom Bubble, VC investment is on the decline. The industry is likely to benefit from continue tailwinds over the long run as the digital economy continues to increase as a % of GDP.

|

|

|

|

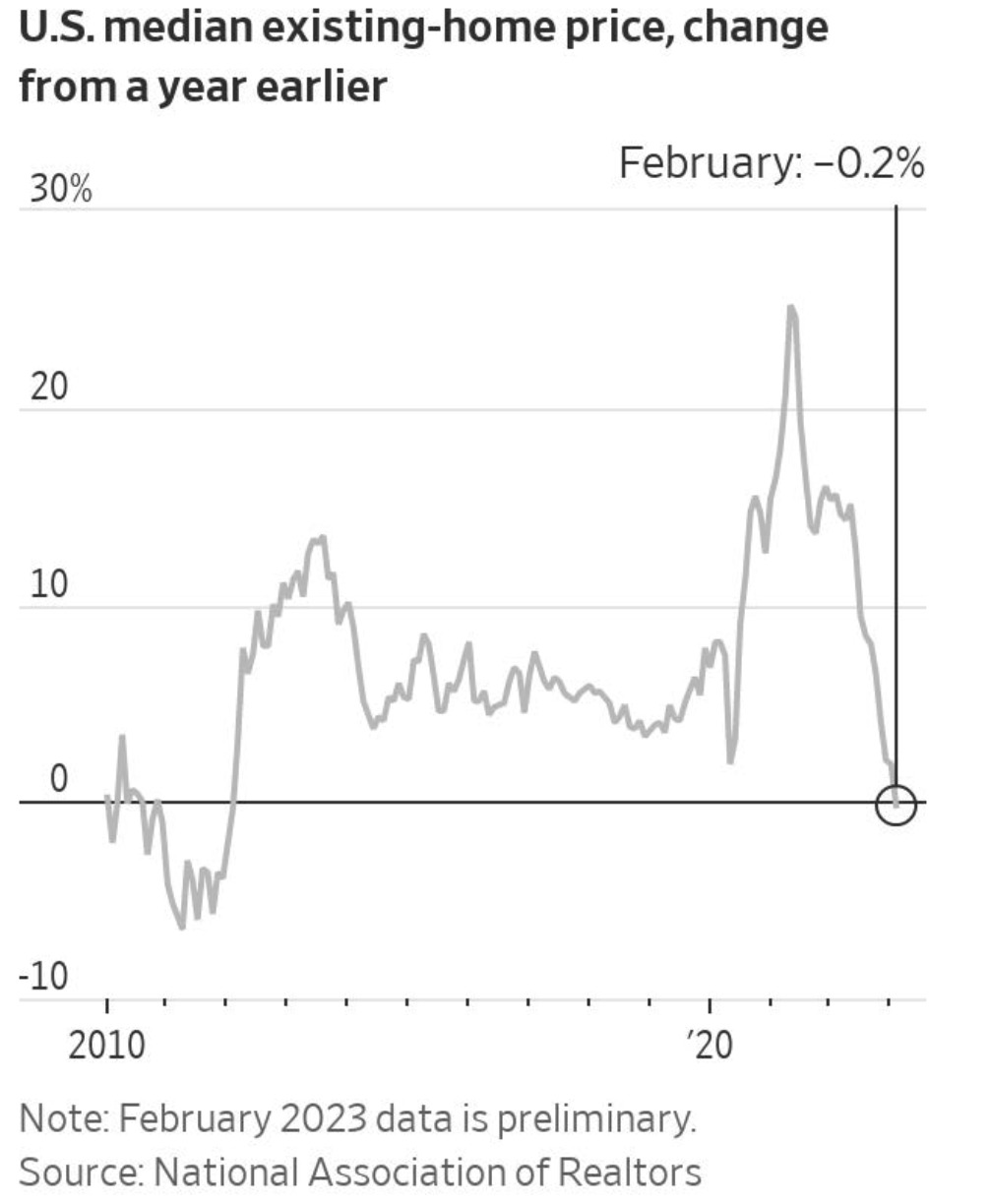

Housing Market Downturn. The U.S. median existing home price fell slightly on a year-over-year basis in February for the first time since 2012 as high mortgage rates crimped affordability and put a damper on buyer demand.

|

|

|

|

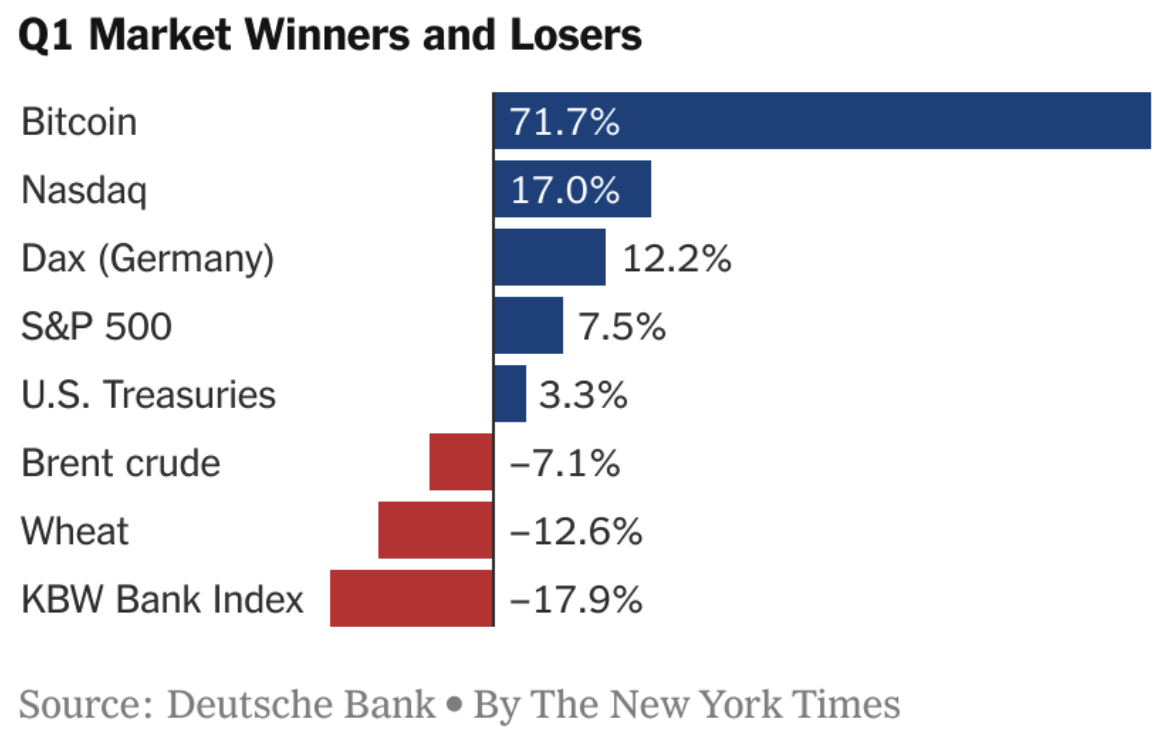

Winners and Losers. Bitcoin was among the best-performing assets during the first quarter with a 72% increase, while the banking crisis ushered in by the collapse of Silicon Valley Bank drove the KBW Bank Index down 18% for the quarter.

|

|

|

|

|

By The Numbers

|

|

|

- $13 trillion: estimated boost to global GDP from AI by the end of the decade, according to the U.S. Chamber of Commerce

- $8 trillion: amount of U.S. uninsured deposits at the end of 2022, up nearly 41% from the end of 2019

- $7 trillion: According to Moody’s Analytics, closing the gender pay gap would boost the global economy by 7%, or $7 trillion

- $2.3 trillion: amount of so-called excess savings accumulated by U.S. households in 2020 and 2021, according to the Fed

- $2 trillion: amount of global private equity dry powder as of 1/3/23, compared to $600B global VC dry powder as of the same date

- $1.6 trillion: federal student debt held by 40 million U.S. borrowers

- $600 billion: market capitalization lost by the 50 largest tech companies that went public since 2020, nearly 60% of their combined market value, according to CB Insights

- $500 billion: estimated hit to venture capitalists’ portfolios related to the fallout from the Silicon Valley Bank collapse

- $211 billion: Silicon Valley Bank’s assets at the end of 2021, up from $116 billion a year earlier

- $193 billion: amount Volkswagen plans to invest in electric vehicles over the next five years as it seeks to hit its target of 50% electric vehicle sales globally by 2030

- $161 billion: Saudi Aramco profit in 2022, a record

- $54 billion: amount borrowed from the Swiss Central Bank by Credit Suisse before its takeover by arch rival UBS

- $8 billion: reported size of IPO for Arm, the Softbank-owned semiconductor intellectual property company, at a potential valuation exceeding $50 billion

- 2.5 billion: number of times the Johns Hopkins Covid-19 map was viewed before it was retired

- 158 million: number of passengers expected to travel for spring break this year, surpassing 2019 levels, according to Airlines for America

- 19 million: number of viewers who tuned into the Oscars this year, the third-worst showing on record

- 311,000: number of U.S. jobs added in February, well above economist expectations for 225,000 new jobs added

- 118,000: number of workers in U.S.-based tech companies have been laid off in mass job cuts so far in 2023, per Crunchbase News

- $42,000: typical U.S. homebuyer down payment in January, the lowest in almost two years, according to Redfin

- 9,000: additional corporate and tech layoffs planned by Amazon by the end of April, adding to the 18,000 roles it already cut late last year and this January

- $2,132: typical monthly mortgage payment for the median U.S. existing home in February ($415,000 price), up 49% from a year ago

- 132: at the pace employers are moving, it will take 132 years to achieve pay equity

- 105: number of hours Miami residents lost to traffic jams in 2022, on average, up 30% from 2019, according to mobility data company Inrix

- 56: Number of countries in the Commonwealth of Nations celebrating Commonwealth Day on March 13

- 11: number of applications used by the average office worker on the job, with 17% using 16 or more apps, according to Gartner’s 2022 Digital Worker Survey

- 92%: percentage of managers who prefer their teams to work onsite, according to a Robert Half survey

- 79%: percentage of respondents in Fannie Mae’s National Housing Survey who said that buying conditions were bad in February, with only 20% saying it was a good time to buy

- 66%: percentage of all leisure and hospitality jobs held by women

- 44%: percentage of 2022 U.S. venture-backed technology and healthcare IPOs

- 41%: obesity rate among U.S. adults ages 20 to 44 in 2020, up from 33% in 2009

- 34%: increase in outstanding consumer debt held by borrowers age 18 to 29 between the first quarter of 2021 and the fourth quarter of 2022, compared to an 11% increase for those 40 and up

- 30%: percentage of U.S. spending attributable to Millennial and Gen Z consumers in 2021, up from approximately 25% in 2019, according to the Labor Department

- 28%: percentage of total days worked from home in February, compared to an average of 30% in each month of 2022, 60% in May 2020, and < 5% before the pandemic

- 13%: percentage of current job postings related to remote positions, down from 17% in March 2022 but well above the prepandemic level of 4%

|

|

|

|

|

|

|

|

|